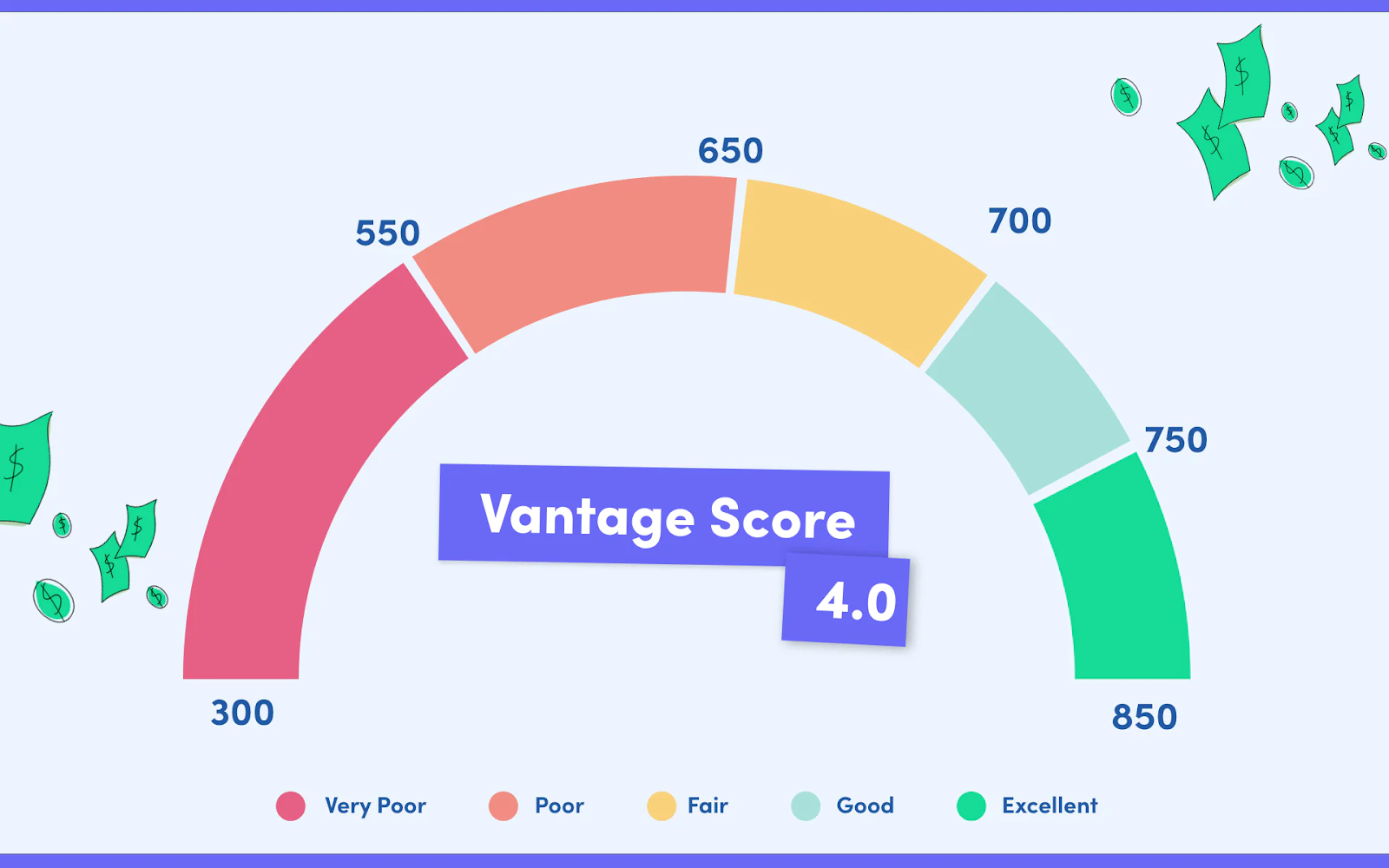

Fannie Mae and Freddie Mac now officially accept VantageScore 4.0 for mortgage underwriting—effective immediately. This marks the most significant credit scoring shift in over a decade, and it is happening now.

Use It Today—No System Changes Required

Lenders can now use VantageScore 4.0 alongside current GSE accepted scoring models for GSE-backed loans. Tri-merge remains in place, meaning there’s no disruption to your LOS or credit reporting setup.

Key Takeaways

- GSE-approved and live for use today

- Broader scoring model that includes consumers with limited credit history

- Built on trended data and machine learning for deeper credit insights

- Tri-merge setup remains valid—no technical changes required

- A strategic moment to evaluate workflow alignment and vendor support

What This Means for Lenders & Brokers

- Lenders may begin submitting VantageScore 4.0 immediately

- Tri-merge reports are still accepted—bi-merge implementation is not yet required

- Increased regulatory and operational focus may lead lenders to revisit vendor alignment and credit strategy

- This is a timely opportunity to confirm that your systems and partners are prepared to support both scoring models efficiently

Birchwood Is Ready

We’ve been preparing clients for this transition for over a year. Whether you need to align processes, review workflows, or simply talk through what this means for your team—we’re here to help.

We offer a quick 15-minute strategy call to walk through the impact—no pitch, just a plan. Book Your Call Here